After an unprecedented amount of economic damage caused by the early stages of global pandemic, today the DJIA hit a milestone, surpassing 30,000 for the first time in its history.

How is this possible? Well, the Fed.

Over the past 8 months, the Federal Reserve has been creating “moral hazard” in financial markets, as it certainly seems as if stocks can never go down. This is despite main street being hampered with further shutdowns and bankruptcies.

Currently, just about every measure of valuation is predicting low to negative returns over the next decade.

While this does not necessarily mean that every year will be negative, it suggests we are likely to witness increased volatility and more frequent declines. As Michael Lebowitz, CFA recently noted:

“Regardless of the economic environment, taking significant risks, and accepting pitiful expected returns is a bad idea. However, there is one more factor we must consider. The Federal Reserve supplies a massive amount of liquidity, much of which is finding its way into the asset markets.

The Fed will likely continue as long as inflation is held at bay. The result may be that stock prices continue to rise, and valuations eclipse all prior norms. However, the music will stop someday, and the facts presented here will be apparent.

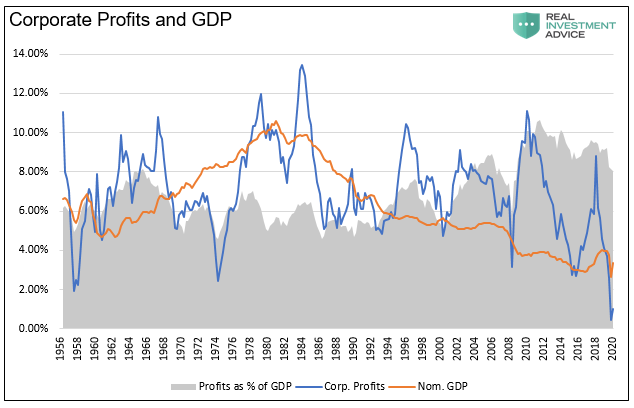

If we take a look at corporate earnings, we can expect stock valuations being based on a multiple of expected future earnings. Expected future earnings are determined by future economic activity. If economic growth is slower in the future, then logically, corporate profits will also be slower. As shown below, corporate profits and economic growth are well correlated.

Thus far, we have established that economic growth is likely to be lower than it was in the past decade (even before COVID-19, markets were slowing). Therefore, we can also assume that corporate profit growth will be weaker than in the past decade.

To add insult to injury, the Biden administration’s $2 trillion tax plan is expected to further hamper corporate earnings, as a 39.6% top marginal rate and 0.9% Medicare surcharge on high incomes will disincentive highly skilled professionals to work longer, innovate more, or assume additional responsibility to advance within their organizations. Productivity is key for increased profits, and may begin to falter when these tax plans take rise.

As such, 2021 is likely to be a challenge.

Currently, the Fed is continuing to supply liquidity to the system (which helps the market ignore valuations, technical deviations, and excessive bullishness), however, when when the Fed decides to takes its foot off the throttle, lower economic growth, gigantic debt overhead, and rich valuations will begin to ripple.

There are a tremendous number of things that can go wrong in the months ahead. Such is particularly the case of a surging stock market against weakening fundamentals. Even with the GSA (the General Services Administration, which supports the basic functioning of federal agencies) having allowed Biden’s presidential transition to begin, risk still remains.

Here is the link to the The MoneyShow: Investing In 2021, aimed at helping investors understand this risk, and how to best avoid it.

Works Cited:

https://www.zerohedge.com/markets/investing-when-markets-detach-economy